DizzyyCO

Financial Guru

Follow for financial Advice personalised for you

Subscribe to Our Email

Blogs

Affiliate Partners

💬 Let’s Be Honest — Budgeting Gets Overcomplicated (But It Doesn’t Have to Be)

Over the years of working in personal finance and helping people clean up their financial chaos, I’ve seen one common theme: most people don’t budget because they think it’s too complicated.

If you’ve ever opened a spreadsheet, panicked, and slammed your laptop shut—I get it. Budgeting gets a bad reputation. But it doesn’t have to be stressful, restrictive, or full of complex tracking systems.

One of the simplest, most effective strategies I recommend to anyone just starting out is the 50/30/20 rule. It’s a beginner-proof framework that helps you manage your money without giving up the things you love—and without needing a finance degree to make it work.

In this post, I’ll walk you through exactly how the 50/30/20 rule works, how to implement it into your life, and how to start using it right away to take back control of your money.

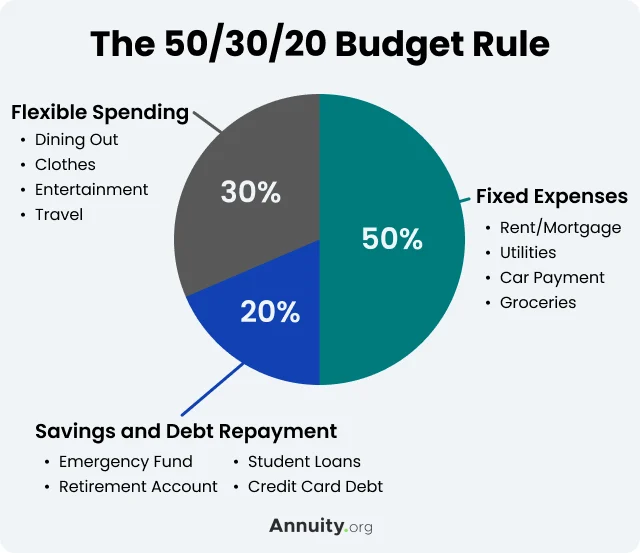

📊 What Is the 50/30/20 Budgeting Rule?

The 50/30/20 rule is a budget structure that divides your after-tax income into three categories:

-

50% for Needs – the non-negotiables

-

30% for Wants – the flexible, fun stuff

-

20% for Savings & Debt Repayment – the key to building your financial future

It’s straightforward, easy to apply, and incredibly powerful when done consistently. This is the exact framework I’ve taught to clients, used in my own life, and seen help people finally feel confident managing their money.

Let’s break down what actually goes into each of these categories.

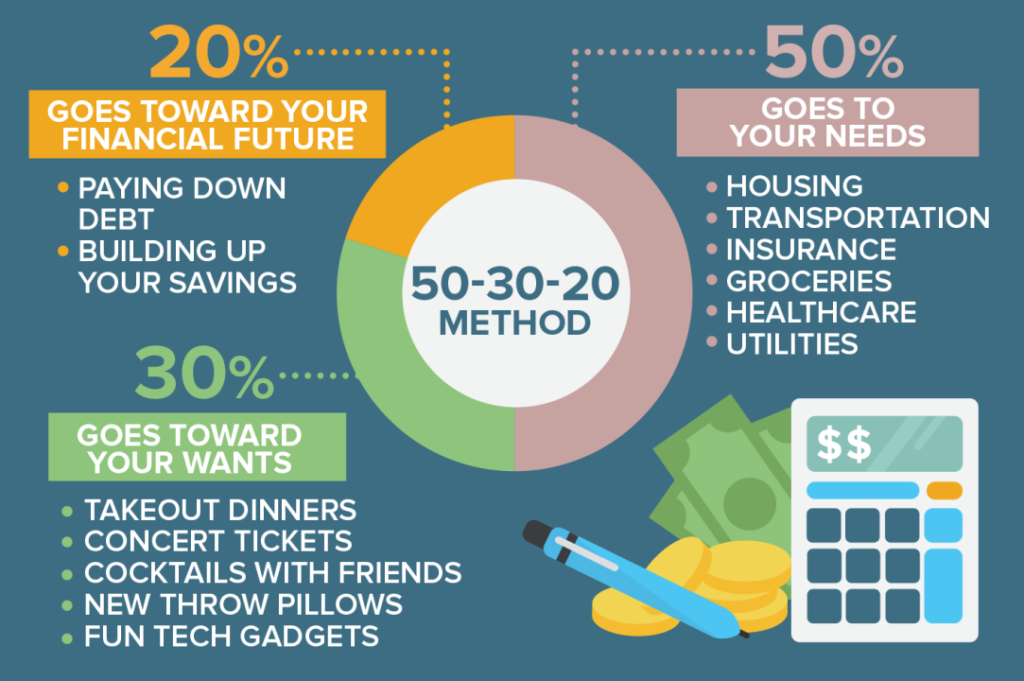

💼 50% for Needs: Covering the Essentials

Needs are your non-negotiable living expenses—things you must pay to maintain your home, health, and livelihood.

Includes:

-

Rent or mortgage

-

Utilities (electricity, gas, water, internet)

-

Groceries (basic food—not takeout or Starbucks runs)

-

Car payments, fuel, or transit costs

-

Insurance (health, auto, etc.)

-

Minimum payments on loans and credit cards

📝 Pro Tip: If your needs category is over 50%, that’s not unusual—especially if you live in a city or support a family. The key is to be aware of where your money is going and adjust elsewhere to make space.

🎉 30% for Wants: Lifestyle & Enjoyment (Yes, You’re Allowed!)

Wants are where we often overspend—and where we feel the most guilt. But in this budgeting method, you’re not cutting them out—you’re planning for them. Guilt-free.

Includes:

-

Dining out and coffee runs

-

Travel and entertainment

-

Subscriptions (Netflix, Spotify, Audible)

-

Shopping, self-care, hobbies

-

Gym memberships, classes, upgrades

📝 Pro Tip: Use a monthly “fun money” cap. When the wants budget is used up, pause and wait until next month. This keeps spending in check without making you feel deprived.

💸 20% for Savings & Debt Repayment: The Long-Term Game

This is the most empowering part of your budget—it’s where financial freedom starts. These funds help you build security, reduce stress, and prepare for the unexpected.

Includes:

-

Emergency fund contributions

-

Extra payments on high-interest debt

-

Retirement savings (IRA, 401(k), etc.)

-

Investments

-

Sinking funds for future big expenses (vacation, house, car)

📝 Pro Tip: Start small. If saving 20% feels impossible, start with 5–10% and work your way up. Progress is more important than perfection.

✅ How to Start Using the 50/30/20 Rule in Real Life

Here’s a 5-step method I walk people through when implementing this structure:

1. Calculate Your Take-Home Income

This is your net income—what actually lands in your bank account after taxes and deductions.

2. Audit Your Current Spending

Look at your last 1–2 months of expenses and group them into needs, wants, and savings/debt. You can use tools like Mint, YNAB, or even your bank’s built-in tools.

3. Run the Numbers

Multiply your income:

-

Needs = x 0.50

-

Wants = x 0.30

-

Savings/Debt = x 0.20

For example, if you bring home $4,000/month:

-

Needs: $2,000

-

Wants: $1,200

-

Savings/Debt: $800

4. Make Strategic Adjustments

If your needs are too high, look at reducing fixed expenses or supplementing income. If your wants are bloated, prioritize what brings you the most value.

5. Automate & Track

Set up automatic transfers to savings and use budgeting tools to stay on track with your plan each month.

💡 Real-Life Example: Budget Breakdown for a Single Professional

Income: $4,200/month after taxes

| Category | Amount | Notes |

|---|---|---|

| Needs (50%) | $2,100 | Rent, groceries, car payment, utilities |

| Wants (30%) | $1,260 | Dining out, weekend trips, skincare, Netflix |

| Savings/Debt (20%) | $840 | Roth IRA, credit card payoff, vacation fund |

This is a sustainable budget that allows room for joy and progress toward long-term goals.

📈 The Benefits of Using the 50/30/20 Rule

If you stick with this framework—even loosely—you’ll start to see real results within a few months. Here’s what I’ve seen happen with my readers and clients:

✅ Less emotional spending

✅ Reduced debt and financial stress

✅ Faster savings growth

✅ More confidence in making money decisions

✅ Freedom to spend without guilt

Plus, it works whether you’re salaried, freelance, or earning side hustle income. You just need a consistent method to track and adjust.

🔁 What If My Budget Doesn’t Fit These Percentages?

This is one of the most common questions I get—and the answer is simple:

The 50/30/20 rule is a guide, not a prison.

If your needs take up 60% or more of your income, you’re not doing it “wrong.” You’re simply working with your current reality. The beauty of this method is that it helps you see clearly and make gradual shifts.

🧩 Some ways to adjust:

-

Cut small recurring subscriptions

-

Eat out 1–2 fewer times/month

-

Negotiate bills (cell phone, insurance, internet)

-

Increase your income with a side hustle

-

Move some “wants” into free or low-cost alternatives

Every dollar you save gives you more breathing room—and that’s what good budgeting is all about.

🧠 Final Thoughts: Simple Rules, Strong Results

The 50/30/20 rule isn’t a magic formula—but it’s one of the most practical, beginner-friendly systems I’ve ever used. And I’ve seen it change lives.

You’ll stop wondering where your money went.

You’ll stop feeling guilty every time you spend.

You’ll start making progress—real, measurable progress—toward the life you actually want.

If you’ve struggled with budgeting before, give this method a try for the next 90 days. You might be surprised by how much clarity and freedom it brings.

DizzyyCO

Financial Guru

Follow for financial Advice personalised for you

Subscribe to Our Email

Blogs

Affiliate Partners

Leave a Reply